Let's Talk

Request a private consultation. Discover how you can Make Your Move™.

Where are opportunities and risks in this deal?

The giveaway guide to identify if a target is a good investment quickly.

DownloadFailed mergers and acquisitions (“M&A”) deals impose significant deadweight and reputational costs on purchasers and targets. Think about the time, blood, sweat and tears spent by deal teams working up to the point when the deal breaks down. The bad news is – failed deals are not uncommon. Deals involving public targets have a significantly higher deal failure rate (11.1%) than those involving private targets (3.7%) according to Intralinks’ report, Abandoned Acquisitions: Why Do Some Deals Fail to Complete.

Deal breakers are often caused by a due diligence oversight. Of all the mistakes that can cause a deal to break down, one of the common ones we keep hearing is that purchasers assume that an audit will reduce deal risk. Nothing can be further from the truth. An audit does not reduce deal risk, i.e. communicate if a purchaser is likely to receive the value paid for.

An audit provides assurance that management has presented a true and fair view of a business’ financial performance and position according to the accounting rules. For a purchaser to make a well-informed investment decision, however, he/she should understand that an audit is a complement to, rather than a substitute for, a specifically tailored financial due diligence investigation of the investment target.

When due diligence is conducted, potential investors are provided with a level of comfort. It would be short-sighted to make an investment decision relying purely only on a target’s audited financial statements since an audit is an opinion on its historical financial performance. However, purchasers are interested to buy into a target’s financial future. Audited financial statements on their own do not address significant issues of interest to prospective investors. This is an important point to both a purchaser and seller. A purchaser wants to know if they will receive future profits and cash flows promised by the seller. This is when financial due diligence is warranted. Due diligence investigates historical and forecasted financial data to answer that question.

Is financial due diligence a different term for an audit? Unfortunately, not! The misconception that finance due diligence is a form of audit arises because they are similar in some ways. Both involve an in-depth investigation and analysis of the target’s company that is to be acquired.

To illustrate the difference between an audit and financial due diligence. imagine that you would like to buy a car. The seller provides you with a vehicle inspection certificate from a reputable mechanic. The purpose of this certificate is to assure you of the car’s roadworthiness.

While having a certificate is nice, you may insist on performing your own ‘due diligence’. You can personally inspect the car, and even take it for a test drive. You listen for any strange sounds or see if you can identify any leaks. Alternatively, you may wish to hire your own mechanic. Your mechanic is familiar with this type of car, its operating history and behaviour. As a professional, he can identify which areas tend to give trouble and analyse the maintenance records. This is to find out if the paperwork is incomplete and/or if accident records have been omitted. These investigations give you a professional view to reduce your chances of buying a lemon.

The financial due diligence provider is that second mechanic. The due diligence provider can tailor the scope of an engagement. The aim is to address specific concerns and risks. We list below 7 key differences between financial due diligence vs an audit.

exhibit 1: seven reasons why due diligence is not audit

A financial due diligence answers different questions compared to an audit. Both services have completely different objectives as shown in the exhibit above An auditor is trained differently from a financial due diligence specialist. Financial due diligence investigates a company’s historical data to explain what drives financial performance. The purpose is to provide an investor with an understanding of the business to make an investment decision. This is not the purpose an audit. An auditor is hired to provide a fairness opinion. An audit does not address investment risks and how to mitigate them. The purpose of an audit is to form a view as to whether the historical financial statements provide a true and fair view according to a regulatory benchmark, i.e. financial reporting standards. There is no regulatory standard for financial due diligence.

Due diligence procedures are tailored according to the industry a target is in, as well as a business’ return vs risk profile. As there is no universal standard to reference, an experienced due diligence specialist selects procedures that focus on what is important to a purchaser. Such questions include:

After investigating these questions, a purchaser should be able to weigh the pros vs cons, e.g. deal breakers, and be able to come to an investment decision.

Due diligence is a guiding light through a complex deal process. Its purpose is to add value and reduce risk. Due diligence efforts involve a range of disciplines depending on how complex a deal is. These include financial, tax, legal, commercial, operational, human resources, technology, etc. Financial due diligence, often also referred to as ‘accounting’ due diligence, focuses on providing investors with an understanding of a business, particularly in the following areas of focus:

If you think that the points above do not resemble an audit conversation, you are right. Audits analyse historical financial information to understand if they are fairly presented based on accounting rules. Financial due diligence, on the other hand, assesses transaction risk. An audit does not to assess the five points above, which are necessary to provide a basic understanding of a deal. A due diligence report is akin a vehicle inspection certificate from a reliable and reputable mechanic to certify the roadworthiness of a car, prior to its purchase.

Financial due diligence, when done correctly, provides a purchaser the insights required to make a go/no go investment decision. It answers questions any investor will ask. For example, what is the basis of the seller’s representations in respect of financial returns promised through ownership of the target?

A financial due diligence exercise helps unearth issues that could potentially derail a transaction. Reducing such risks could mean the difference between a profitable vs unprofitable deal. More importantly, a good financial due diligence report helps M&A lawyers protect purchasers in case what the seller promises does not come true. Given that more than 60% of M&A deals fail to deliver the value promised[1], it is critical that investors and lenders have the confidence to finance a transaction. Stock exchanges are also increasingly demanding independently produced (1) financial due diligence and (2) business valuation reports as a sign of good corporate governance.

Sellers must ensure that a target’s financial information is accurate. This helps a seller communicate the true worth of his business and justify his asking price. More importantly, it prevents him from being sued for misrepresentation. Although many sellers choose to have a financial audit of their company, it typically does not include all the information that a buyer is interested in knowing before making an acquisition decision.

Due diligence is a part of every M&A deal. A seller who is clear about due diligence improves a target’s marketability, increases credibility with the buyer, and helps to decrease the transaction timeline. A vendor due diligence report prepared on behalf of a seller before a purchaser appear can give peace of mind that key issues, analyses and validations of all the commercial, operational, financial, and strategic assumptions of interest to a purchaser has been addressed ahead of time.

A purchaser will only invest if he is comfortable with the target and is confident that it will give him the investment return he seeks. Financial due diligence allows a purchaser to verify the accuracy of the information and representations provided by the seller. Since the report shows the story beyond the numbers, a buyer is able to make a more informed decision by identifying the risks, liabilities, and opportunities.

Purchasers typically request us to focus on one more of the following areas:

Quality of business information

This provides an overview of the business. Information includes an overview of the business model, key accounting policies, corporate milestones, shareholder, officers, product lines and geographies, etc.

Quality of earnings

A quality of earnings report helps to establish the value of a business by analyzing and reporting on detailed aspects that may not be readily identifiable to a seller, buyer or investor in reviewing the financial statements.

Quality of earnings refers to the proportion of income attributable to the core operating activities of a business. Thus, if a business reports an increase in profits due to improved sales or cost reductions, the quality of earnings improves. A high quality of earnings is important to investors since they have a right to enjoy earnings distributions from a business.

Quality of net assets

Net assets are what a company owns outright, minus what it owes. Net assets provide a rough guide for the value of company resources. A quality of net assets analysis helps establish the worth and condition of assets, liabilities, contingencies and off-balance sheet items. Typically, the higher a company’s net asset value, the higher the value of a business.

Quality of cash flow and working capital

It can be argued that operating cash flow is perhaps the single most important figure in a set of financial statements. That’s because it shows how much cash is being generated by the running of the day-to-day business of the company. Profitable, well-run, established businesses generally have consistently positive operating cash flow. Unprofitable, poorly run businesses generally do not.

Quality of forecast

Companies that produce timely, comprehensive Cash Flow Statements are usually better at forecasting future cash flows. This is because how actual cash flows have been generated is a useful starting point to validate the credibility of projected future cash flows.

This also allows for ongoing “actual versus budget” comparisons of cash flows as part of the company’s monthly reporting. Forecasted cash flows are important as they provide purchasers a guide as to when and where they can expect a return on investment.

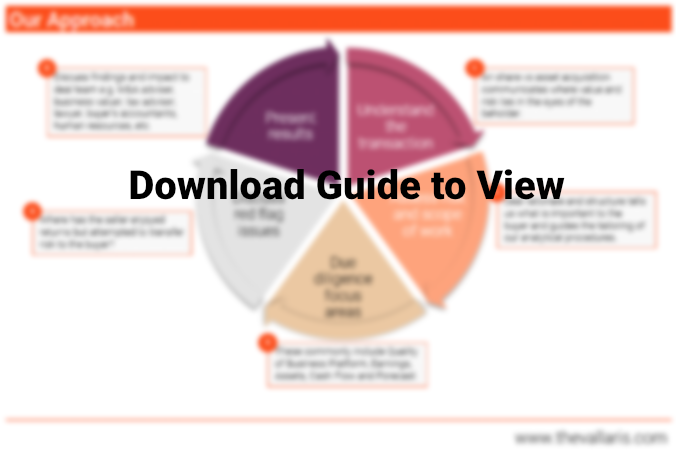

exhibit 2: VALLARIS’ due diligence process

VALLARIS’ financial due diligence process is a proven 5 step framework that covers the following:

1. Understand the transaction

Understand a purchaser’s deal objectives. This helps us understand why he wants to do this deal, what his priorities and deal breakers are. We use that understanding to tailor of a scope of work that addresses these concerns and provide the clarity he needs to make a go/no go investment decision.

2. Assess risk and scope of work

As risk is in the eye of the beholder, there is no one size fits all scope of work. An experienced financial due diligence specialist must be able to translate a holistic view of deal risk by first understanding how to establish what is important to a purchaser and his concerns. We suggest investigation procedures that address industry and business specific risks. A due diligence specialist will translate available data, information and the unique processes to provide a big picture, quantify key opportunities and mitigate risks.

3. Due diligence focus areas

Participants of failed deals will tell you that they could have turned the tide if only they had more budget and resources for due diligence. The reality of deal-making is that it is a time pressured, messy, non-linear affair. Purchasers are often provided information that is incomplete, and poor in both quality and quantity. It is the job of the due diligence specialist to prioritize focus areas that have the most outsized impact to providing clear deal optics and reducing risk.

4. Discuss red flag issues

Which are the key issues that drive deal opportunity and warn of danger? Can risks be mitigated so that a purchaser can receive investment returns? Due diligence that uncovers and addresses red flags quickly is essential to deal closure success. Purchasers have to strike while the iron is hot. The longer a deal drags out, the colder the opportunity becomes, the less interested both parties become in working with each other. The honeymoon phase is short in M&A and once the sparks wear-off, the marriage doesn’t last, especially since it hasn’t even been consummated yet.

5. Present results

When we refer to quick due diligence, we mean presenting results between 30 and 60 days after the term sheet is signed. 90 days is not ideal, but–from our personal experience–anything north of 90 days does not bode well for ensuring a high probability for deal closure.

Every business has skeletons, but the key is to uncover and address them before a purchaser invests, not after. Lack of attention to ongoing due diligence can lead to missed deal breakers. It also results in unbudgeted liabilities and the diversion of the time and energy of key executives. Most the required documentation can be provided quickly, but feet-dragging is the natural state of most sellers. As an advisor representing the seller, it’s our duty to eliminate such a tendency and pace the deal.

Financial due diligence equips both seller and buyer the strategic confidence to transact. Sellers or buyers all over world have requested VALLARIS guide them throughout the transaction process to uncover and minimize deal risk.

Identify deal risk before you sign your cheque.

Request a meeting with VALLARIS.

Reference

[1] https://hbr.org/2016/05/so-many-ma-deals-fail-because-companies-overlook-this-simple-strategy