Let's Talk

Request a private consultation. Discover how you can Make Your Move™.

Auditors face tight deadlines and fee pressures from clients, who are perceived to focus more on the cost rather than the quality of the valuation service.

The giveaway guide to navigate financial instrument valuation reporting confidently.

DownloadHow good is your promise to pay? A financial instrument is a piece of paper known as a monetary contract. It is made between two parties, can be traded and settled. The contract represents an asset to one party (the buyer) and a financial liability to the other party (the seller). Accordingly, you can find them listed on a balance sheet as either a financial asset, financial liability, or equity instrument. You may recognize them as cash, shares or bonds.

In the aftermath of the 2008 global financial crisis, regulators grew increasingly concerned about consumer protection. Over time, the number of new financial instrument types grew in complexity ahead of investor sophistication. The Lehman Minibond crisis showed that many investors who bought such investments did not have a clear understanding of the product’s features. Part of the reason is that such products are quite complex and embed features that are difficult to understand. This suggests that if the inherent risk and the complexity of a product’s structure are not clearly understood by investors, they would not be able to make informed investment decisions.

While not all financial instruments are hard to understand, the truth is it often takes years of specialized expertise and experience to value complex financial instruments.

Let us first describe financial instruments by asset class before discussing how to value them.

An asset class refers to a group of investments that exhibit similar characteristics and are subject to the same laws and regulations. An asset class refers to the form a financial instrument takes, e.g. share, bond, derivative, forex or commodity. Financial instruments can be separated according to asset class and can be further divided by whether they are complex or non-complex.

There are four main asset classes: equities (shares), fixed income (bonds), cash equivalents, and alternative investments (commodities, real estate, financial derivatives, private equity). Different asset classes react differently to news. For example, if there was news of a recession, equities prices may fall, while investment-grade debt and alternative investment, e.g. gold, prices may rise.

exhibit 1: financial asset classes

Equities

Equity instruments are shares in the ownership of a business. There are several types of equity instruments:(a) Common (ordinary) shares represent a partial ownership of the company. This type of share gives the stockholder the right to share in the profits of the company, and to vote on matters of corporate policy and the composition of the members of the board of directors.(b) Preferred shares are financial instruments that represent an equity interest in a company but may not allow its owners voting rights. Preferred stocks are senior (i.e., higher ranking) to common stock, but subordinate to bonds in terms of claim (or rights to their share of the assets of the company) and may have priority over common stock (ordinary shares) in the payment of dividends and upon liquidation.

Fixed income

Fixed income securities are a type of debt instrument. It provides returns by way of regular, or fixed, interest payments. It also repays the principal when the security reaches maturity. These instruments are issued by governments, corporations, and other entities to finance their operations. They differ from equity, as they do not entail an ownership interest in a company, but they confer a seniority of claim, as compared to equity interests, in cases of bankruptcy or default. Examples of fixed income instruments include bonds, Treasury notes (“T-notes”) and Treasury bills (“T-bills”). They are marketable securities sold by a government to pay off debt and raise cash. The difference between each is based on the length of time held by an investor and the interest they pay:

Cash and cash equivalents

Cash and cash equivalents are the most liquid current assets found on a business’s balance sheet. They are short-term, highly liquid investments with a maturity date that was 3 months or less at the time of purchase. In other words, there is very little risk of collecting the full amount being reported.(a) Money market account is a savings account that offers you the potential to earn higher interest than an ordinary savings account.(b) Commercial paper is an unsecured promissory note, as the security is not supported by anything other than the issuer’s promise to repay the face value at the maturity date specified on the note. A commercial paper pays a fixed interest rate to the holder. Also, it is generally sold at a discount to its face value due to the somewhat risky nature of the unsecured security. The need for commercial paper often arises due to corporations facing a short-term need to cover their expenses.

Alternative investments

exhibit 2: alternative asset classes

A non-complex financial instrument is one that can be traded without a great deal of specialist knowledge. Non-complex financial instruments include shares or equity securities, as well as debt securities and certain types of investment funds[1].

Equity securities refer to shares in companies, while debt securities include both government and corporate bonds. Debt securities can also refer to preferred stock and forms of collateralised securities – such as collateralised debt obligations.

Investment funds include hedge funds and mutual funds. These are all instruments which enable investors to pool their money under a specialist who is in charge of the fund: the fund manager.

Complex financial instruments (“CFI”) require an in-depth knowledge for traders to be successful when trading them. Derivatives are a common example of complex financial instruments. Different derivatives have different benefits. For example, contracts for difference (“CFD”) are good for hedging.

Many studies have discussed ‘complexity’ but there is no commonly accepted definition. However, the International Organization of Securities Commissions (“IOSCO”) has provided a useful description of complex financial products. According to IOSCO, complex financial products refer to financial products:

Financial derivatives are examples of complex financial instruments. These include but are not limited to the following:

Defining a CFI can be a complex subject, let along valuing one. CFIs have distinctive features that need to be considered when valuing the security, such conversion or redemption options, vesting conditions, or embedded derivatives.

Here are five CFI behavioral characteristics that can help us identify a CFI:

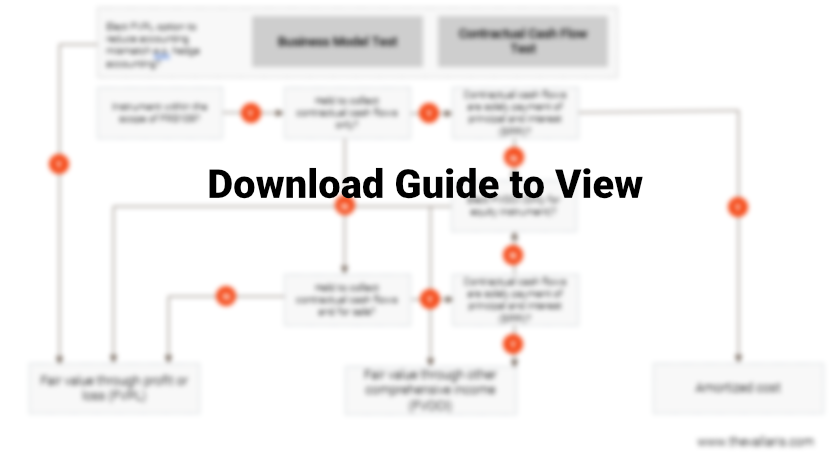

exhibit 3: financial asset classification (two test technique)

exhibit 4: financial asset classification & measurement

1. Leverage: amplifies market exposure relative to an investment in the underlying instrument. Gains and losses are experienced more quickly, sometimes much more quickly, than in an un-leveraged investment. Leverage can take several different forms:

2. Maturity mis-match: Occurs when a company’s short-term liabilities exceed its short-term assets. It can also occur when a hedging instrument and the underlying asset’s maturities are misaligned.

3. Market liquidity: As witnessed during the Lehman Minibond crisis, market liquidity for many of these instruments didn’t just reduce but in some instances ceased to exist. In these circumstances, valuations and price verification for these instruments become challenging as they had limited evidential support.

4. Lack of price transparency: These instruments are often bespoke, and their valuations depend on proprietary financial models and the inputs that drive those models. Frequently, the inputs for these models are not directly observable in the market. In addition, even a valid model with accurate inputs will not always capture the immediate supply and demand profile of the market, meaning that the model price will not always determine the price at which a transaction will occur. In this circumstance, buyers and sellers may achieve price discovery only through actual transactions. Transactions which in this case are hard to come by.

5. Path reliance The returns at maturity assume that underlying assets’ features take certain future paths, i.e. price risk, event risk. A valuation must therefore include a robust simulation of possible outcomes or paths. Repeat calculation could give a more accurate payoff result.

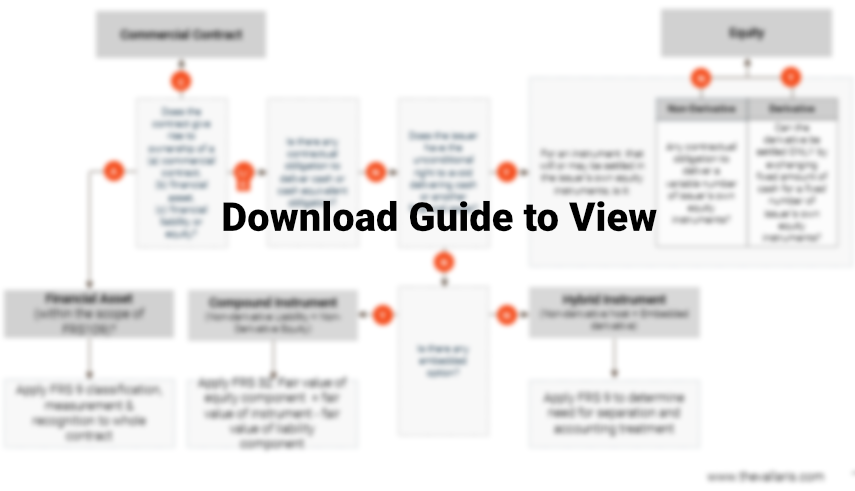

exhibit 5: compound vs hybrid instrument

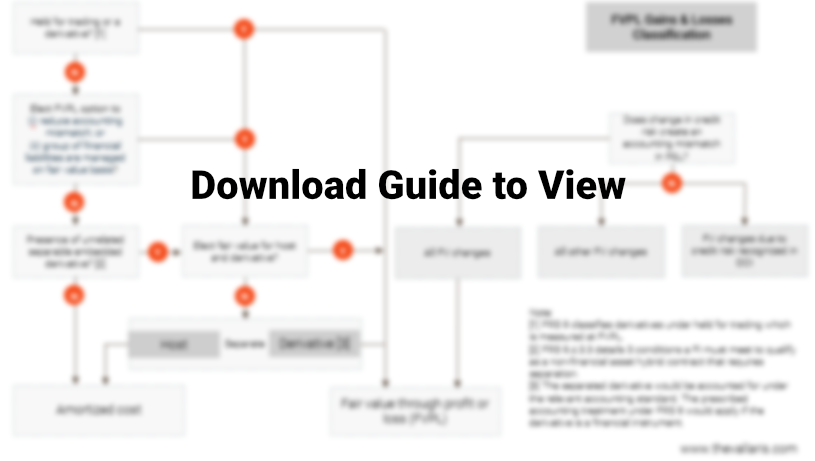

We list below suggestions on how to fair value different types of financial instruments:

Financial instruments are a growing presence on company balance sheets, and business executives say more market awareness is needed to prevent another financial crisis, according to a recent survey by the American Institute of CPAs (AICPA)[2].

When asked about the complexity, their level of concern about the valuation and reporting of financial instruments, respondents provided the following responses:

Complex financial instruments historically have been difficult to value. That difficulty is seen as a major cause of the financial crisis that led to the recession of 2008. Creating standard processes for documenting and valuing these instruments will improve clarity and transparency. This in turn enhances confidence from capital markets and stakeholders.

Maintain stakeholder trust with accurate asset values.

Request a meeting with VALLARIS.

Reference

[1] European Securities and Markets Authority, Markets in Financial Instruments Directive II (“MiFID II”) Directive 2014/65/EU, Annex 1, Section C

[2] https://www.aicpa.org/content/dam/aicpa/interestareas/businessindustryandgovernment/newsandpublications/downloadabledocuments/2q-2019-eos-es.pdf