What is Share-based Payment?

Share-based payment (“SBP”) is a transaction in which an entity acquires or receives goods and services for equity-based payment. These goods can include tangible assets like property or inventory, intangible assets, and other non-financial assets.

A business may supplement cash compensation by awarding to employees shares of the business or the right to buy shares of the business. SBP are great tools for rewarding employees of the business for meeting a performance target, remaining loyal and in more broader terms creating wealth for shareholders.

Share-based payment valuation explains to employees what payments are worth in cash.

Mun Siong Yoong, Founder & CEO

How Do Share-based Payments Work?

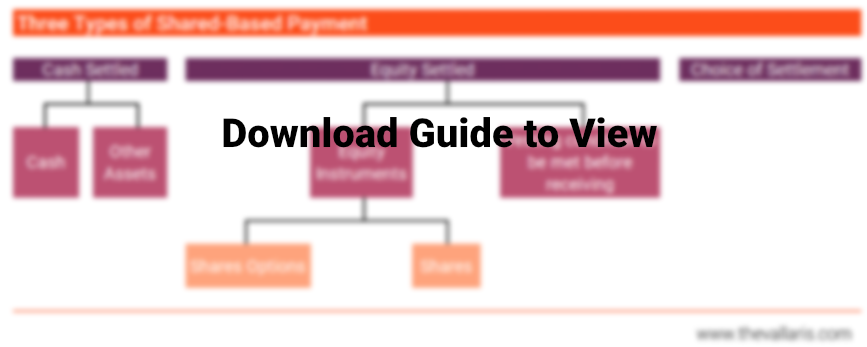

There are three (3) types of share-based payment arrangements between an entity and a counterparty (including an employee).

exhibit 1: types of share-based payment

Cash-settled share-based payment arrangement

- The counterparty receives cash or other assets of the entity for amounts that are based on the price (or value) of equity instruments (including shares or share options) of the entity or another group entity.

Equity-settled share-based payment arrangement

- The counterparty receives equity instruments (including shares or share options) of the entity or another group entity.

- If there are certain specified vesting conditions, these must be met before receiving any share-based payment.

- Choice of settlement share-based payment arrangement:

- This includes transactions of which either the entity or the counterparty has a choice of settlement (to receive equity instruments or cash / other assets).

How Do You Audit Share-based Payments?

The auditor evaluates the appropriateness of the accounting treatment and ensures that the share-based payments are recognised and measured in accordance with FRS 102. In addition, the auditor assesses both the accuracy of the option-pricing model calculations, and the appropriateness of the underlying data used as inputs in the model, including the assumptions made by management. In practice, the nature and extent of the work done by the auditor also depends on whether the fair value has been determined by management or an external valuation specialist.

Some of the key audit procedures typically performed include:

- Evaluate appropriateness of the valuation method selected by the entity by considering whether it is applied in a manner consistent with FRS guidance and economic theory, and reflects the substantive characteristics of the share-based payment arrangement in question;

- Obtain copies of spreadsheets with the valuation calculations, perform checks and re-compute for mathematical and theoretical accuracy;

- Hold discussions with management and external valuation specialists engaged, if applicable, to understand any specific assumptions made for inputs to the valuation, and corroborating such assumptions (for example, expected term of options, share price and expected volatility, expected dividends), and

- Assess the systems, and related controls, that generate the data used in the fair value computations, including share option/ share award systems (for example, records of grants, forfeitures, lapses, exercise) and payroll/ HR systems (for example, employee numbers, employment contracts, length of employment, attrition rates).

Relying on audit work performed by parent company:

- Arrangements where a parent company grants shares or share options to employees of a subsidiary can present additional practical challenges for the auditor of the subsidiary. The extent to which the subsidiary auditor can rely on audit work performed by the parent company auditor requires judgement.

- Generally, the subsidiary auditor would not rely solely on the parent company auditor, but would also request and review copies of the relevant workings, reconcile amounts within them to both the subsidiary and parent company financial statements, review statements issued to employees, and obtain relevant confirmations from the employees and the parent company as to completeness. It may also be possible to access and review the parent company’s share-based payment systems, or the working papers of the parent company auditor, but such arrangements require early communication. The subsidiary auditor should bear in mind that the parent company auditor is likely to work with a higher materiality threshold.

Engaging an expert to assist in the review of the valuation of share-based payments:

- According to SSA 620 Using the Work of an Auditor’s Expert, whenever expertise in a field other than accounting or auditing is necessary to obtain sufficient appropriate audit evidence, the auditor must consider whether to engage an auditor’s expert e.g. a business valuer.

- In order to decide when to engage an expert, the engagement partner takes into consideration, among others, the complexity of the valuation performed, the significance of the amounts involved, whether the management has engaged a management’s expert, and their competence and capabilities.

- Auditors should consider the potential impact of FRS 102 on their clients at an early stage of the audit since the audit of share-based payment is likely to involve other professional parties, including valuation specialists and/or auditors of the parent. This will allow the auditors sufficient time and effort to perform an effective and efficient share-based payments audit.

Common Issues in Accounting for Share-based Payments

Common issues include:

- For equity-settled share-based payments, changes in share price after grant date do not affect the accounting treatment.

- In contrast, for cash-settled share-based payments, the accounting treatment reflects changes in share price after the grant date because those price changes affect the amount of cash that the entity must ultimately pay.

- For equity-settled share-based payments, changes in share price after the grant date does not affect the fair value measured as at grant date. This is consistent with accounting treatment for other obligations that must be settled by issued equity instruments as payment, which reflects that the value of services is unlikely to change in line with subsequent changes in share prices

- There is some degree of complexity in determining vesting conditions of share‑based payments and how the valuation is impacted.

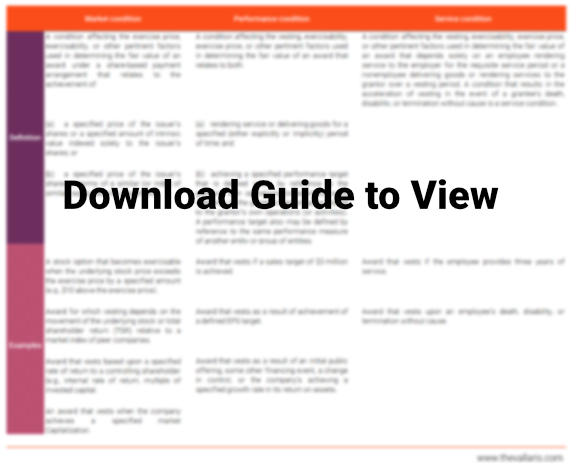

- FRS 102 defines three (3) types of vesting conditions:

- Market condition

- Performance condition

- Service condition

Definitions and examples:

exhibit 2: vesting conditions

Market conditions

- A share award with a market condition is accounted for and measured differently from an award that has a performance or service condition.

- The effect of a market condition is reflected in the award’s fair value on the grant date (e.g., using an advanced option-pricing model, such as a binomial model).

- That fair value will be lower than the fair value of an identical award that has only a service or performance condition because the effect of the market condition results in a discount relative to the fair value of an award without a market condition. All compensation cost for an award that has a market condition should be recognized if the requisite service period is fulfilled, even if the market condition is never satisfied (i.e., even if the award never vests). This is because the likelihood of achieving the market condition is incorporated into the fair value of the award.

Performance and service conditions

- For a share award with a performance and/or service condition that affects vesting, the performance and/or service condition is not considered in determining the award’s fair value on the grant date.

- For companies that elect to estimate forfeiture rates, service conditions are considered when a company is estimating the quantity of awards that will vest (i.e., the pre-vesting forfeiture assumption). The share-based payment expense reflects the number of awards that are expected to vest and will be adjusted to reflect those awards that ultimately vest.

How is Share-based Compensation Calculated?

Fair value should be based on market price wherever this is possible. Because observable market prices are generally not available for employee stock options, companies need to use an option-pricing (or equity valuation) model to estimate the fair value of employee stock options and other employee equity awards, such as restricted stock with market conditions.

The best-known valuation techniques are:

- Black-Scholes-Merton (Black-Scholes) model,

- Monte Carlo simulation models, and

- Binomial models.

While the choice between the Black-Scholes, Monte Carlo simulation, and binomials models is important, the fair value estimates produced by any of these techniques are largely dependent upon the assumptions used. The assumptions usually have a greater impact on fair value than the choice of model. The Black Scholes is likely to be the first choice for entities performing inhouse valuations, but it may not be appropriate for all types of share-based payment schemes.

For example, the Black-Scholes model requires adjustment if the options can be exercised prior to the maturity date; share options that include market performance conditions are generally better valued with a Binomial valuation or Monte Carlo simulation.

Companies are permitted to select the option-pricing or equity valuation model that best fits their unique circumstances as long as the valuation technique:

- is applied in a manner consistent with the fair value measurement objectives of FRS 102;

- is based upon established principles of financial theory;

- reflects all of the substantive terms and conditions of the award.

As a result, for most employee stock options and other employee equity instruments, companies have flexibility in selecting the option-pricing or equity valuation model used to estimate the fair value of their share-based compensation schemes.

The Black-Scholes model is relatively simple to use and well understood in the financial community. Its relative simplicity stems, in part, from the fact that when estimating the fair value of an employee option, all expected employee exercise behaviour and post-vesting cancellation activity is reduced to a single average expected term assumption. The principal advantage of binomial models, on the other hand, is that they accommodate a wider range of assumptions about employees’ future exercise patterns, as well as accommodate other assumptions that may change over time. This approach may yield a more refined estimate of fair value. A Monte Carlo model simulates a very large number (as many as 1,000,000) of potential stock price scenarios over time and incorporates varied assumptions about volatility and exercise behaviour for those various scenarios. A fair value is determined for each potential outcome. The grant date fair value of the award is the average of the fair values calculated for each potential outcome.

For awards with typical service conditions and performance conditions, the Black-Scholes model will generally produce a reasonable estimate of fair value. Monte Carlo simulation and binomial models result in a more refined estimate of fair value. Additionally, companies that issue awards with market conditions or payoff conditions that limit exercisability should use either a Monte Carlo simulation model or a binomial model because those models can better incorporate assumptions about exercisability in relation to the price movements of the underlying stock and/or potential payoff outcomes related to achievement of market conditions.

Companies need to weigh the advantages and disadvantages of each model in order to choose a model that fits their particular circumstances. In deciding which model is most appropriate, some factors to consider are:

- Design of the share-based compensation plan

- The specific terms of awards granted by a company may have an impact on which option-pricing or equity valuation model it selects. For example, it is generally appropriate (and common practice) for most “plain vanilla” stock options to be valued using the Black-Scholes model.

- However, binomial models are sometimes used for other awards, including options that are in-the-money, awards with market conditions, and awards with payoff functions limited in certain ways e.g. as maximum value options.

- It is common practice for a Monte Carlo simulation model to be used when valuing awards containing a market condition.

- Data availability

- The principal advantage offered by Monte Carlo simulation and binomial models is that they can accommodate a wider range of assumptions; however, this poses certain challenges. Companies may need to analyse a significant amount of detailed historical employee exercise behaviour in order to develop appropriate assumptions required by a binomial model or a Monte Carlo simulation model. Many companies may not have the necessary historical data, or may conclude that their history is not relevant in making assumptions about future exercise patterns. Thus, the Black-Scholes model may be more practical, assuming it is appropriate for the type of award.

- Cost–benefit analysis

- Although the Monte Carlo simulation and binomial models may provide a more refined estimate of fair value for some award types, companies should weigh the costs involved before switching from the Black-Scholes model. Some companies may determine that the costs of applying a Monte Carlo simulation or binomial model outweigh the benefits of a more refined fair value estimate.

Companies may decide to change from one option-pricing or equity valuation model to a different one (e.g., from Black-Scholes to a binomial model). A change in option-pricing model is not a change in accounting principle—the underlying objective of estimating the fair value of the award is the same — and therefore does not require justification of preferability. However, changes in valuation models should generally only be made when the new model will result in an improved estimate of fair value. Additionally, companies may use one model for certain awards and another model for different types of awards. For example, the fair value of a “plain vanilla” option could be estimated using the Black-Scholes model while a Monte Carlo simulation is used for an option with a market condition.

How Does Share-based Payment Impact Your Financial Statements?

FRS 102 requires an expense to be recognised for the goods or services received by a company. The corresponding entry in the accounting records will either be a liability or an increase in the equity of the company, depending on whether the transaction is settled in cash or in equity shares. Goods or services acquired in a share-based payment transaction should be recognised when they are received. In the case of goods, this is the date when this occurs. However, it is often more difficult to determine when services are received. If shares are issued that vest immediately, then it can be assumed that these are in consideration of past services. As a result, the expense should be recognised immediately. Alternatively, if the share options vest in the future, then it is assumed that the equity instruments relate to future services and recognition is therefore spread over that period.

Get Help

Find it a challenge to retain great employees? Get the value of share payments right.

Request a meeting with VALLARIS.